Review the latest Weekly Headings by CIO Larry Adam.

Key takeaways

Recent tech headlines have stirred up fresh disruption fears, weighing on software stocks and the sector more broadly. Below, we break down key takeaways from 4Q25 earnings and share our latest views on tech:

4Q25 earnings season momentum continues its strong drive

4Q25 earnings season is off to a strong start. So far, over 70% of the S&P 500’s market cap has reported results, and earnings are on track to rise roughly 13% year over year – up from just 7% at the start of earnings season. This marks the fifth consecutive quarter of double-digit EPS growth, a streak last seen in 2018. To date, roughly 80% of companies are beating estimates – above the five-year average – and in aggregate are surpassing forecasts by roughly 8% - the strongest since 1Q21. Yet, despite strong 4Q25 results, the most notable storylines this earnings season have revolved around rotation dynamics and the recent sell-off in tech stocks.

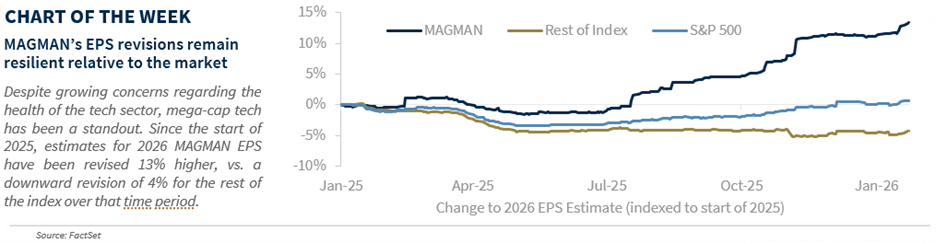

Mega-cap tech has dominated the field

While software has dominated recent headlines, mega‑cap tech has quietly delivered another strong 4Q earnings season. With five of the six mega-cap names (NVDA is still to come) having reported, MAGMAN* is on pace to grow its earnings 26% year over year and has collectively beaten estimates by roughly 8%. Consensus estimates have been revised modestly higher, with upward revisions still outpacing the broader index. 2026 MAGMAN earnings are on track to rise 25% – the fourth straight year outpacing the rest of the S&P 500 Index – and margins are expected to expand to 29%, a four-point increase vs. last year and over double the broader index. Despite more discerning investor sentiment, each of the mega-cap names has raised capex estimates, providing support for AI infrastructure beneficiaries, such as semiconductors. While dispersion within tech will likely persist as AI disruption creates winners and losers, we remain overweight mega-cap tech in 2026, given the still-supportive fundamental backdrop.

AI Is still controlling the playbook

AI is reshaping industries in very different ways, and its momentum keeps accelerating. Despite lingering supply constraints, cloud growth remains strong, and major large language models (LLMs) such as Gemini are hitting record token‑processing levels, underscoring how quickly AI usage is scaling. At the same time, hyperscalers have raised their capex estimates again, with spending now projected to reach $641 billion in 2026, a 58% year-over-year increase. For perspective, that’s roughly the market cap of the 12th‑largest company in the S&P 500 (Exxon Mobil). Importantly, the benefits of AI are spreading beyond tech. Industrial companies are reporting supply‑chain efficiency gains, grocers are seeing better inventory management that supports margin expansion and lower prices, and financial firms are noting improved retention rates and meaningful productivity boosts. The bottom line: AI investment is set to continue – and likely accelerate – as adoption spreads across the corporate landscape.

2026 estimates back a broader team effort in performance

The broadening of market performance has been a standout theme this year, with the S&P 500 Equal Weight Index outperforming the traditional S&P 500 by roughly 4.2%, the widest gap at this point in the year since 1991. While we’re still constructive on tech, the 2026 earnings outlook shows that this broadening is being driven by improving fundamentals. In 4Q25, only one non‑tech sector – industrials – posted earnings-per-share (EPS) growth above 10%. But as 2026 estimates move higher, seven sectors are now expected to deliver EPS growth above 10%, and the median S&P 500 stock is projected to see an acceleration in EPS growth along with margin expansion versus 2025. A strengthening earnings backdrop, paired with corporate commentary highlighting a resilient consumer and expectations for stronger GDP growth in 2026, keeps us optimistic that this broadening can continue and supports our positive long‑term view on the wider market.

Emerging markets are moving the ball

Emerging markets equities are building on last year’s momentum – up roughly 7% year to date and outperforming the S&P 500 by roughly 8%, the widest early‑year lead since 2001. Strong earnings trends have been a major driver: emerging markets earnings for 2026 are on track to grow 29% year over year, the fastest pace since 2010. Upward revisions have been notable, with consensus EPS estimates rising roughly 9% since January, well above the long‑term average. Together with steady inflows, these revisions have helped lift the broader index. Country performance has also stood out. Markets like South Korea and Taiwan – both heavily weighted toward chipmakers and tech hardware manufacturers – are up roughly 23% and 10%, respectively, with improving fundamentals continuing to support their outlook.

*MAGMAN represents a composite of Microsoft, Apple, Google, Meta, Amazon, Nvidia. The foregoing is not a recommendation to buy or sell MAGMAN stocks.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

The S&P 500 Total Return Index: The index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.